LAGOS (Reuters) - Collapsing oil prices have left African producers facing not only lost revenue when they most need it to tackle coronavirus, but also a fall in hard-won market share they may never regain.

FILE PHOTO: The logo of the Organisation of the Petroleum Exporting Countries (OPEC). Vienna, Austria December 6, 2019. REUTERS/Leonhard Foeger/File Photo

The continent’s producers such as Nigeria, Angola and Algeria cannot compete with the lower costs of erstwhile allies Saudi Arabia and Russia, who are flooding the market with oil.

In a sign of their desperation, the Republic of Congo’s oil minister wrote to OPEC secretary general Mohammad Barkindo on March 20 calling for an urgent meeting to find a way to keep member nations from sinking into recession.

But while desperate for OPEC+, the Organization of the Petroleum Exporting Countries plus Russia, to ride to the rescue, Africa’s oil producers have little leverage over them.

“They have no power,” one Nigerian oil industry source told Reuters. “All they can do is ask.”

Although non-OPEC nations such as Britain, Norway and the United States all have relatively high-cost production, their diversified economies mean they are not dependent on oil.

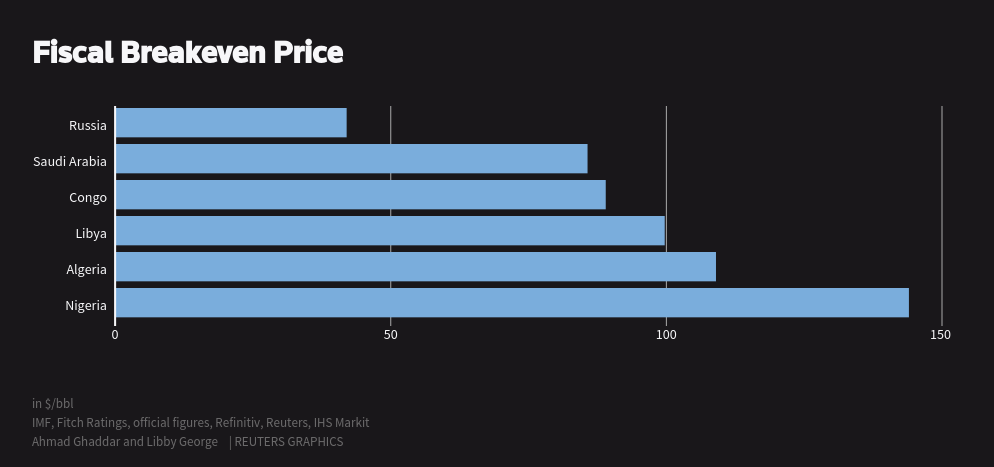

(Graphic: Fiscal Breakeven Price link: here)

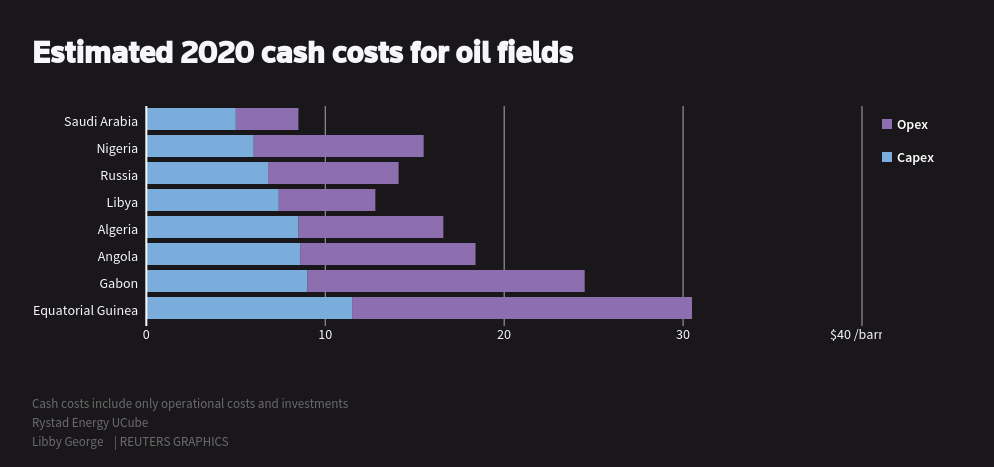

As well as hitting already tight budgets, the oil price drop had led oil majors to cut billions from spending plans. The longer-term impact for the comparatively costly African fields could be far more painful.

(Graphic: Estimated 2020 cash costs for oil fields link: here)

“Companies are reviewing their whole portfolios on a daily basis,” said Roderick Bruce, principal research analyst for Africa at IHS Markit, which forecasts final investment decisions on the continent could hit historic lows this year.

“They (African countries) are in a very difficult position,” Bruce added, citing their higher production costs.

In Nigeria, for instance, production is forecast to fall by 35% without offshore field investments. Across Africa, Rystad estimates delayed spending could mean 200,000 barrels per day (bpd) drop in expected output by 2025.

“The discipline that’s going to be introduced will be a shock to the system,” said Alex Vines, head of the Africa Program at British think-tank Chatham House.

“This is really different terrain, and these are very vulnerable economies,” Vines added.

Larger nations are also elbowing African producers out of incredibly competitive spot trade.

They cannot match the agile, aggressive marketing that saw Saudi Arabia slash its selling prices almost immediately after the collapse of the OPEC+ deal.

By comparison, Nigeria took nearly two weeks to make record cuts to its official selling prices.

The country is also struggling to sell its oil, which is rich in the gasoline and jet fuel that the world is not using as a result of the coronavirus pandemic.

While Angola’s production has fallen from close to 2 million barrels per day (bpd) a decade ago to 1.4 million bpd, it had been in the midst of reforms which were meant to boost output.

And Equatorial Guinea is trying to auction new licenses and find a replacement for ExxonMobil, which wants to leave.

CASH CRUNCH

The sudden cash crunch is also hindering the ability of Africa’s oil producers to manage growing coronavirus outbreaks and a group of African finance ministers has called for a $100 billion stimulus package to help deal with the pandemic.

Health systems across the continent are already chronically underfunded and citizens are often too poor and tightly packed in slums to stock food or self isolate, while the oil crunch also casts doubt on whether nations can craft rescue packages or pay soldiers and police to enforce lockdowns or combat unrest.

Nigeria, which has cut nearly $5 billion from its budget and promised a halt to all non-essential projects, said it needs 120 billion naira ($333.33 million) to fight the coronavirus outbreak.

Algeria, whose public debt rose to 45% of gross domestic product at the end of last year from 26% in 2017, plans 30% public spending cuts and has directed state energy firm Sonatrach to halve planned investment to $7 billion.

(Graphic: African Oil Producer Debt to GDP Ratios link: here)

Angola, where oil production has fallen steadily in recent years, is mulling a $3 billion Eurobond offering to shore up a budget based on $55 per barrel oil, while debt-ridden Congo Republic has been trying to renegotiate $1.7 billion of oil-backed loans.

No comments:

Post a Comment